What Investors Actually Want to See in your Biotech’s Financial Model Before Series B

Key Takeaways:

- Series B investors scrutinize CMC timelines and manufacturing risk more than most founders anticipate

- Licensing obligation stacks can quietly complicate financial projections and reduce deal attractiveness

- Clean, IP-free manufacturing platforms strengthen the defensibility of financial models

- IND readiness and GMP campaign visibility are critical signals of program maturity for institutional investors

- The most fundable programs are those where the path from current stage to clinical proof-of-concept is clearly de-risked

The conversation between a biotech founder and a Series B investor is rarely what either party expects it to be. Founders often prepare for deep engagement on scientific differentiation mechanism of action, competitive positioning, preclinical data packages. Sophisticated institutional investors those who have evaluated dozens of biopharma programs across the development spectrum often surprise founders by quickly shifting focus to a different set of questions entirely.

They want to know about the manufacturing plan. They want to understand the CMC timeline. They want to see where the licensing obligations sit and how they affect long-term revenue projections. And they want to understand whether the path from current stage to a clinical readout is genuinely de-risked or whether it is being presented with more confidence than the underlying facts support.

For founders preparing a biotech Series B financial model CMC investor due diligence package, understanding this dynamic is not optional it is the difference between a term sheet and a polite pass.

Why CMC Has Become a Financial Conversation

Five years ago, CMC was primarily a scientific and regulatory topic. Investors knew it mattered, but the evaluation was typically surface-level: has the company selected a CDMO? Is there a GMP campaign planned? Is the IND timeline reasonable?

That has changed. A combination of high-profile late-stage CMC failures, greater investor sophistication in the biopharma space, and the emergence of specialist due diligence consultants focused specifically on manufacturing risk has elevated CMC scrutiny in the Series B process to a level that most founders are not fully prepared for.

Institutional investors at the Series B stage have typically seen programs fail for reasons that had nothing to do with biology and everything to do with manufacturing. A molecule that could not be expressed at scale. A process that worked at the ten-liter scale in development and fell apart at two hundred liters in GMP. A technology transfer that consumed eighteen months instead of the six that were projected. A licensing obligation that was never fully modelled, which revealed itself during due diligence as a material drag on the financial projections that had been presented to the board.

These are not rare events. They are sufficiently common that experienced life science investors have learned to probe for them specifically.

The Financial Model Elements Investors Will Test

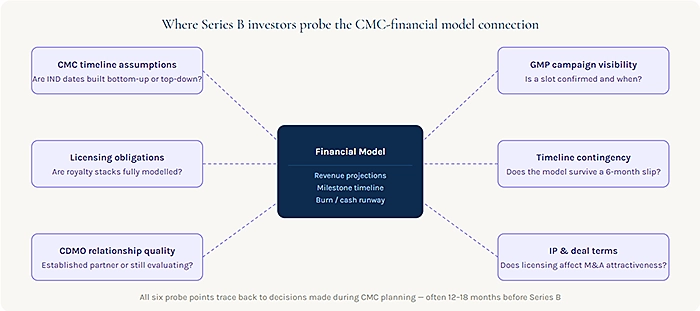

When an investor reviews a biopharma financial model at the Series B stage, they are typically evaluating several layers simultaneously, and the CMC layer is more important than most founders realize.

Timeline assumptions and their downstream dependencies. The financial model projects cash burn, revenue potential, and valuation milestones based on assumptions about when key clinical events will occur. Those clinical events depend on when GMP material will be available. GMP material availability depends on when process development will be complete. All of this sits downstream of the CMC plan. An investor who understands this chain will trace the assumptions backward from the clinical readout date to the current CMC state and ask whether the timeline between the two is genuinely achievable.

Experienced investors know that early-stage CMC timelines are routinely optimistic. Cell line development takes longer than projected. Process development surfaces unexpected challenges. Technology transfers encounter compatibility issues. When a financial model assumes a twelve-month IND timeline from a current pre-IND CMC position, an investor who knows the space will mentally add three to six months and evaluate the model accordingly. If the underlying financial assumptions cannot survive that adjustment, the model has a problem.

Licensing obligations and their downstream financial impact. This is where many biotech financial models have a hidden weakness. The model may project impressive revenue figures in the commercial stage, but those figures often do not fully reflect the royalty obligations attached to core platform technologies. Expression system licenses, cell line technology fees, and manufacturing platform royalties that seemed modest in pre-IND discussions become meaningful percentage points against revenue in the commercial period.

An investor who identifies an unmodelled royalty stack in due diligence will immediately recalculate the projected financials, assess how the obligations affect peak margins, and evaluate whether the terms are sufficiently well-negotiated to preserve the program’s economic attractiveness in a partnership or M&A scenario. Programs that have made deliberate choices to use IP-free or royalty-free manufacturing platforms such as expression systems that carry no milestone payments, royalties, or license fees present a materially cleaner picture. The financial model is simpler, the margin projections are more defensible, and the downstream deal economics are easier to underwrite.

CDMO relationship quality and manufacturing readiness. Investors will look carefully at the nature of the relationship between the biotech and its manufacturing partner. A program that is “evaluating CDMO options” six months before a planned GMP campaign presents a different risk profile than one that has an established development relationship with an integrated CDMO that is already familiar with the molecule and process. The existence of a technical development agreement, preliminary batch records, and a confirmed manufacturing slot is meaningful due diligence evidence that manufacturing readiness is real and not aspirational.

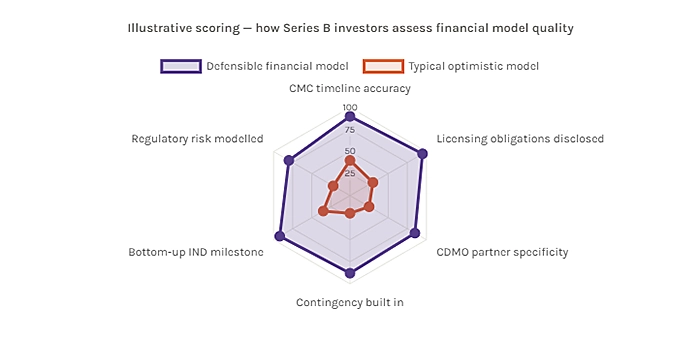

What Separates Defensible Projections From Optimistic Ones

The Series B investors most likely to write a check into a biopharma program are not the ones who will accept projections at face value they are the ones who will pressure-test every assumption and still conclude that the program is fundable. Getting to that conclusion requires that the financial model can survive scrutiny, not just inspire enthusiasm.

Several things distinguish a defensible financial model from an optimistic one in the biopharma context.

The CMC timeline should be built from the bottom up, not the top down. Many financial models set a desired IND date and work backward, allocating time to each CMC workstream to make the math work. Defensible models are built from current CMC state forward, using realistic timelines based on where the program actually is not where it needs to be for the model to tell a good story. The difference between these two approaches is usually visible to an experienced reviewer within minutes.

The licensing obligations should be fully surfaced and modelled. Every technology license in the program should appear in the financial model as a current cost if it carries access fees, and as a future obligation if it carries downstream royalties or milestones. Founders sometimes resist this level of transparency, worried that surfacing licensing costs will raise concerns. In fact, the opposite is true: investors who find licensing obligations during due diligence that were not disclosed in the financial model lose confidence in the overall quality of the management team’s financial oversight.

The manufacturing strategy should be specific, not generic. Financial models that describe manufacturing plans as “working with a top-tier CDMO” without naming a partner, describing the scope of the engagement, or providing timeline milestones are red flags for investors. Specificity signals maturity. Vagueness signals that the manufacturing plan has not been developed to a level that justifies the timeline it is assumed to support.

The Narrative That Closes Rounds

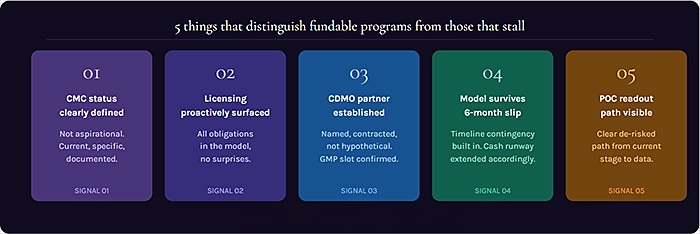

Beyond the numbers, a Series B raise in biopharma is ultimately a narrative exercise. Investors are deciding whether they believe in the management team’s ability to execute a specific plan under conditions of scientific and operational uncertainty. The financial model is the evidence for that belief and evidence needs to be internally consistent, externally defensible, and honest about the risks that remain open.

The programs that close Series B rounds efficiently tend to have a few things in common. Their CMC status is clearly defined and their manufacturing plan is specific enough to be evaluated. Their licensing obligations have been proactively addressed either by selecting IP-free platforms or by negotiating terms that are clearly documented and modelled. Their CDMO relationship is established, not hypothetical. And their financial model reflects a realistic path from current stage to clinical proof-of-concept, without the optimism gaps that experienced investors will find and flag.

None of this guarantees a close. Drug development is inherently uncertain, and investors know that. What it does is establish the kind of credibility operational credibility, financial credibility, CMC credibility that makes investors comfortable enough to bet on the team even when the science is still unfolding.

That credibility is built long before the Series B road show begins. It is built in the decisions made during platform selection, CDMO evaluation, and CMC planning often a year or more before any institutional investor gets involved. Founders who understand that are building toward a fundable program from the beginning, not preparing for fundraising at the last minute.

Preparing your program for institutional investment? The CMC and licensing elements of your financial model deserve as much attention as the clinical and commercial projections. Get the assumptions right early, and the story takes care of itself.

{kind=link}